With Zoe Zhang and Richard Knight, Execution Quant Group, CLSA

At the institutional brokerage division of CLSA, trading China is a key focus for us across trading desks. Our team of quants is always looking for ways to improve performance; one way we can accomplish this is by optimizing execution during the “Closing Phase”, a distinct period in Chinese markets which begins on average 40 minutes before the closing bell.

Algorithmic suites need to dynamically detect the beginning of the Closing Phase and adjust trading patterns to optimize execution outcomes during this critical period. At CLSA we do exactly this. Once we have spotted a pattern to the Closing Phase, we are likely to investigate further, and during this phase, many stock-specific trading factors used by CLSA’s ADAPTIVE trading algorithms change markedly.

CLOSING PHASE IDENTIFICATION

In Chinese equity markets, thin auction volumes on both Shanghai and Shenzhen exchanges force traders who are targeting the close to start executing their order early. This creates an observable microstructure change and commences the distinct Closing Phase.

We have studied a large number of microstructure metrics, attempting to identify features that show a noticeable and repeatable change in the run up to the closing auction.

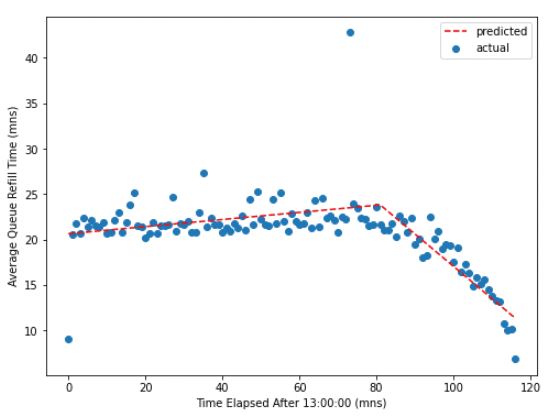

One such metric is order book refill time, or the average time taken for the quote size to be depleted. The average exchange profile for this feature is shown in the figure below.

By using the multivariate adaptive regression spline (MARS) modelling technique, we can identify the point at which this microstructure change occurs — on average, approximately 40 minutes before the close of trading.

There are a number of China-specific microstructure constraints that lead us to believe this feature is a good proxy for behavioral changes related to close trading. These include regulatory restrictions on the placement-to-cancellation ratio; odd lot fills; and conflated market data.

When calculating the total volume traded within the Closing Phase, we find that this brings mainland markets much more in line with other developed markets at around 20% of full-day volume (compared with <1% in the actual closing auction).

It is important to note that while Closing Phase effects can be expected to occur at roughly the same time each trading day, the exact timing will vary based on the amount of participants targeting the close, as well as the liquidity of the stock.

IMPLICATIONS FOR TRADING STRATEGIES

Our analysis indicates that the microstructure characteristics within the closing phase are markedly different than those observed earlier in the trading day.

One notable difference comes from evaluation of the market impact coefficients which are significantly lower than in the pre-close phase.

Some implications for algorithmic trading strategies are as follows:

Relying on daily averages to assess microstructure characteristics is insufficient. Algorithmic suites must be able to detect and adapt to intraday trading phases.

The reduced market impact in the closing phase should be taken into consideration when calculating optimal schedules targeting Close, VWAP or IS benchmarks.

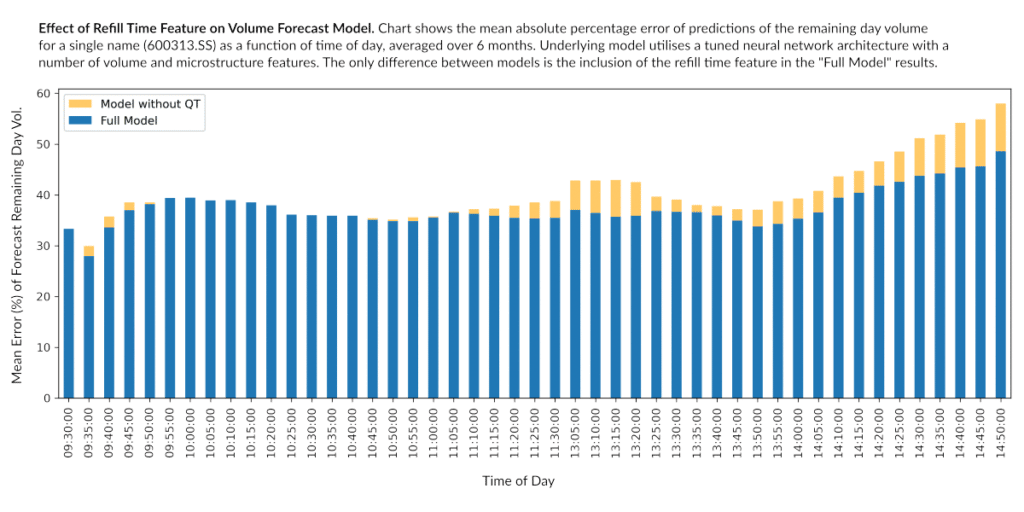

Real-time deviations in key microstructure metrics can be an important indication of the amount of trading targeting the close. As such, they can provide unique and differentiated features for improving the performance of volume and alpha prediction models (see example of volume forecast model below).

Within the Closing Phase, strategies can price orders more passively, maximizing spread capture with lower chance of adverse selection.

SUMMARY

From careful observation of microstructure trading metrics, it is possible to identify changes in participant behaviour that we believe relates to trades that target the close. These changes define a Closing Phase that brings the percentage of volume targeting the close much more in line with other developed markets. Several key microstructure features show a noticeable change during this period; we believe it is key for execution strategies to react to these changes in real time to ensure optimal execution.

At CLSA we recognize that the pattern in trading China is evolving, and market participants need to adapt. We have embedded this discovery not only in our CLOSE Algo to markedly improve performance against the benchmark, but also into our entire ADAPTIVE suite to provide a broader trading edge.

DISCLAIMER: This publication is subject to and incorporates the terms and conditions of use and disclaimers set out on www.clsa.com/disclaimer.html